Staggered Payouts Clear the Way for the Social Security May 27 Distribution

Strategic Balancing: How the May 27 Social Security Administration Payment Calendar Impacts May 2026 Beneficiaries

The Social Security Administration distributes monthly retirement, disability, and survivor benefits to more than 71 million Americans using a highly structured, staggered framework. This comprehensive guide clarifies how the federal agency manages these critical financial disbursements, specifically detailing the eligibility criteria for the upcoming May 27 distribution window. By examining the structural layout of the federal payment calendar, beneficiaries can safely track expected fund arrivals, identify potential banking delivery lags, and effectively plan their households’ monthly financial obligations.

Direct Matrix: Detailed Federal Distribution Architecture for May 2026

The Social Security Administration (SSA) relies on a mechanized distribution protocol designed to balance processing strain across banking infrastructures while ensuring reliable financial access for beneficiaries. Under this regulatory model, disbursements are divided into distinct weekly tranches governed by the recipient’s birth date or specific program onboarding history.

For the current month, the traditional three-Wednesday rotation cycle operates without holiday interruption, following the explicit timelines outlined by the federal agency.

May 2026 Federal Benefit Distribution Roster

| Distribution Target | Specific Eligibility Criteria | May 2026 Distribution Date |

| Supplemental Security Income (SSI) | Low-income aged, blind, or disabled individuals | Friday, May 1, 2026 |

| Pre-May 1997 Beneficiaries | Onboarded prior to May 1, 1997, or concurrent SSA/SSI | Sunday, May 3, 2026 |

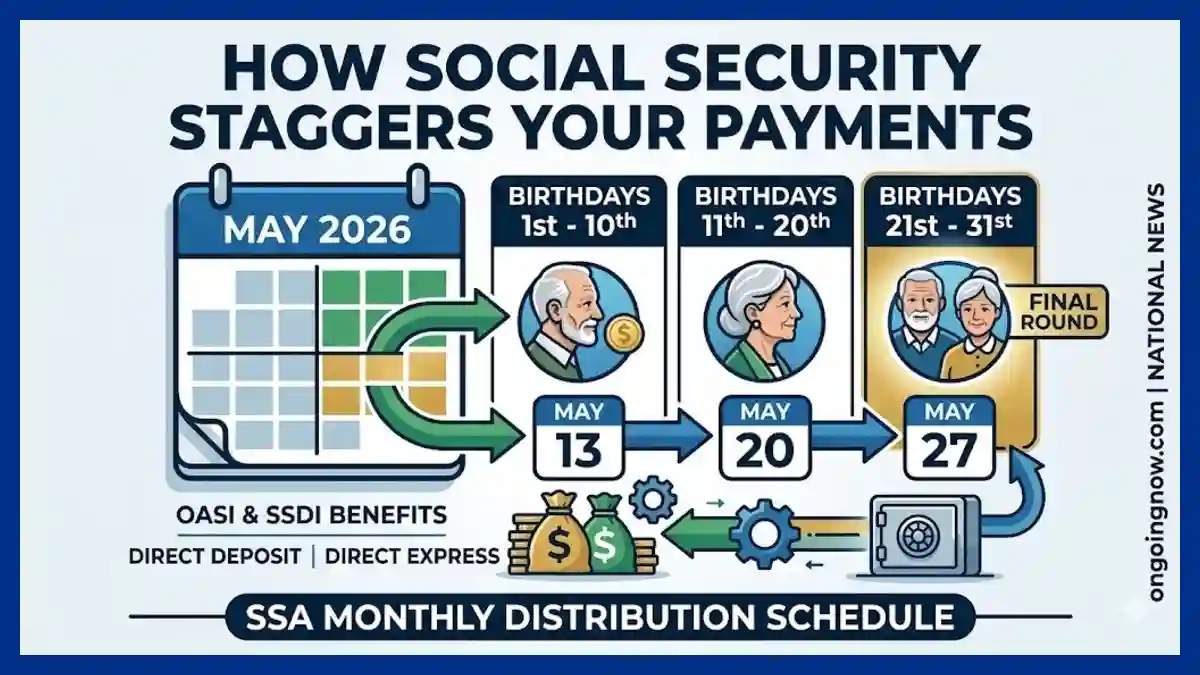

| First Wednesday Tranche | Birthdays falling between the 1st and 10th of any month | Wednesday, May 13, 2026 |

| Second Wednesday Tranche | Birthdays falling between the 11th and 20th of any month | Wednesday, May 20, 2026 |

| Third Wednesday Tranche | Birthdays falling between the 21st and 31st of any month | Wednesday, May 27, 2026 |

Operational Caveat: While the official SSA schedule dictates fixed processing dates, actual local availability depends strictly on individual commercial bank clearing cycles, processing bottlenecks, and direct deposit enrollment parameters.

Institutional Framework: Navigating the May 27 Distribution Window

The final operational cycle of the current monthly schedule concludes on Wednesday, May 27, 2026. This targeted processing date specifically services beneficiaries whose birth dates fall between the 21st and 31st of any given month. Individuals within this birth date range receive their Old-Age and Survivors Insurance (OASI) or Social Security Disability Insurance (SSDI) benefits directly on this day, provided they were enrolled in the federal program after May 1997.

Administratively, this staggered system prevents the Federal Reserve’s automated clearing house networks from experiencing operational delays that could emerge if 71 million disbursements occurred simultaneously. According to official SSA guidance, the distribution incorporates the current 2.8% Cost-of-Living Adjustment (COLA) implemented at the start of the fiscal period, adjusting the average individual monthly payout to maintain baseline household purchasing power.

Technical Analysis: Calculating Monthly Individual Benefit Scale

The individual value of a monthly retirement disbursement is fundamentally governed by historical lifetime earnings, payroll tax contributions, and the exact age at which a beneficiary formally filed for federal benefits. The agency updates its structural maximum thresholds annually to reflect shifts in national wage indexes and economic adjustments.

Social Security Average and Maximum Caps (Fiscal Year 2026 Data)

Average Monthly Retired Worker Check: $2,081.16

Average Monthly Disability Benefit (SSDI): $1,493.20

Average Monthly Survivor Benefit: $1,625.56

Maximum Benefit at Early Retirement (Age 62): $2,969.00

Maximum Benefit at Full Retirement Age (FRA): $4,152.00

Maximum Benefit at Delayed Retirement (Age 70): $5,181.00

Financially, delaying claims past the statutory Full Retirement Age provides an incremental credit increase up to age 70. This operational reality creates a wide financial spread between early-career claimants and individuals who maximize their career contributions up to the maximum annual taxable limit ($168,600).

Operational Mechanics: Verifying Electronic Funds and Identifying Payment Delays

The Department of the Treasury strictly mandates electronic disbursements for all modern federal benefit programs to minimize processing overhead and eliminate logistical failure points associated with paper mailings. Recipients utilize either a standard personal banking institution via direct deposit or a government-issued Direct Express debit card to secure their monthly allocations.

[Federal Reserve ACH Processing File Launched]

│

▼

[Scheduled Distribution Date]

│

┌──────────┴──────────┐

▼ ▼

[Direct Deposit Verified] [Potential Delivery Delay]

(Immediate Fund Access) (Check Clearing Bottlenecks)

│

▼

[Await 3 Business Days]

│

▼

[Contact SSA Bureau]

When checking electronic portals, beneficiaries must observe institutional variations. Private financial providers and fintech organizations frequently utilize provisional processing systems to credit accounts up to forty-eight hours before the official federal clearing day. Consequently, standard commercial bank customers should not anticipate matching these early access timelines, as institutional policies dictate adherence to the formal automated settlement dates.

Analytical Evaluation: Administrative Action Steps for Processing Deviations

The Social Security Administration advises that short-term direct deposit variances are typically driven by local financial processing queues or localized banking network updates rather than federal funding constraints. If an expected electronic deposit does not register on the morning of May 27, beneficiaries are directed to systematically verify their account status before escalating their inquiry to a local field office.

The official federal directive requires all program recipients to allow exactly three full business days for institutional settlement before contacting an agency representative. For the May 27 distribution, this operational window extends through the conclusion of the subsequent week, factoring in traditional business operating hours. Regional processing networks handle high volumes during mid-week transitions, meaning account updating sequences can naturally vary by several hours depending on individual geographic locations.

Community Impacts: The Critical Nexus of Staggered Timelines and Household Budgets

The rigid execution of the federal birth date distribution framework has measurable socio-economic implications for communities nationwide. Because payouts are parsed out uniformly across consecutive weeks, consumer spending patterns, utility payments, and grocery retail demand fluctuate reliably according to local beneficiary demographics.

Families relying entirely on these fixed incomes build their micro-budgets around these designated Wednesdays. While a three-week staggered delay ensures administrative safety and processing stability for the government, it requires strict internal accounting from households managing fixed payment deadlines for housing, municipal utilities, and medical costs.

Historical Policy Precedent: The Structural Evolution of Staggered Payouts

The contemporary layout governing federal benefit delivery dates dates back to an administrative overhaul implemented in June 1997. Prior to this regulatory adjustment, the Social Security Administration distributed all retirement and disability checks on the third calendar day of each month, a legacy practice that routinely overwhelmed tracking mechanisms, regional logistics, and banking teller networks.

By splitting post-1997 beneficiaries into three distinct regional or birth-date-based groups, the federal government successfully modernized the financial safety net’s delivery model. Individuals who maintained their active status prior to May 1997 were legally grandfathered into the legacy cycle, which explains why a segment of older retirees continues to receive funding on the third of each month, preserving long-standing historical processing continuity.

Stay sharp with Ongoing Now!

Source and Data Limitations: This policy explainer relies entirely on official publications, legislative releases, and statistical data sheets issued by the United States Social Security Administration (SSA) updated through May 2026. Figures regarding average benefit values, distribution schedules, and programmatic limits originate directly from the April 2026 SSA Monthly Statistical Snapshot and the formal 2026 Schedule of Social Security Benefit Payments (Publication No. 05-10031). Specific financial limit projections reflect verified legal benchmarks associated with the 2.8% Cost-of-Living Adjustment (COLA) enacted for the current fiscal period. This text deliberately omits all unverified commercial banking processing timeline commitments, regional postal performance speculations, and unconfirmed legislative proposals regarding future programmatic structural reorganizations.