Who Qualifies for Trump IRA? Why Income Limits Matter

Analyzing the shifts in retirement policy, income limits for federal matches, and how middle-income households are adapting.

The traditional image of retirement planning often involves a solitary worker contributing to a corporate 401(k), but for many Americans in 2026, that reality has shifted toward more flexible, government-supported models. As living costs remain a primary concern for households, the introduction of updated retirement incentives has prompted a significant re-evaluation of how families allocate their monthly earnings. This shift is particularly evident as individuals look toward the latest federal frameworks to understand who qualifies for Trump IRA benefits and how these accounts integrate with existing savings habits.

The move toward these accounts reflects a broader trend in personal finance: the transition from purely employer-led retirement to a hybrid model involving direct federal participation. For a freelance graphic designer or a part-time retail associate, the question of eligibility is no longer just about what a boss offers, but about how their specific income level aligns with national thresholds. Understanding these nuances is essential for anyone navigating the current economic landscape where inflation and wage growth continue to interact in unpredictable ways.

Recent data from the Bureau of Labor Statistics (BLS) and the Internal Revenue Service (IRS) suggests that a growing segment of the workforce is now prioritizing “portable” retirement options. As policy updates from the Treasury Department take effect this year, the focus has landed squarely on those in the “middle-income” bracket. This group often finds themselves earning too much for certain subsidies but not enough to feel fully secure in their long-term financial outlook, making the specific limits of new retirement vehicles a critical point of study.

The Landscape of Modern Retirement Eligibility

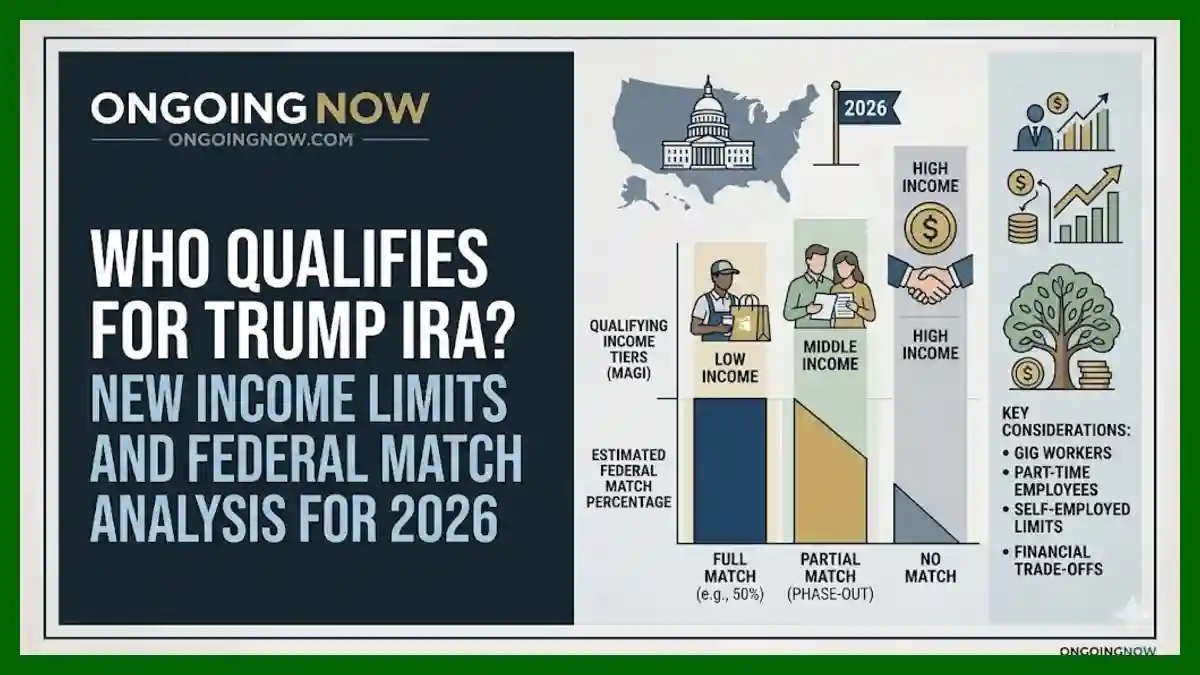

The criteria defining who qualifies for Trump IRA participation are rooted in a combination of employment status and specific income benchmarks. Unlike traditional pension plans of the past, these accounts are designed to be accessible to a wider variety of workers, including those who do not have access to a workplace-sponsored plan. This inclusivity addresses a long-standing gap in the American retirement system where gig workers and part-time staff were often left to save without any form of matching contribution.

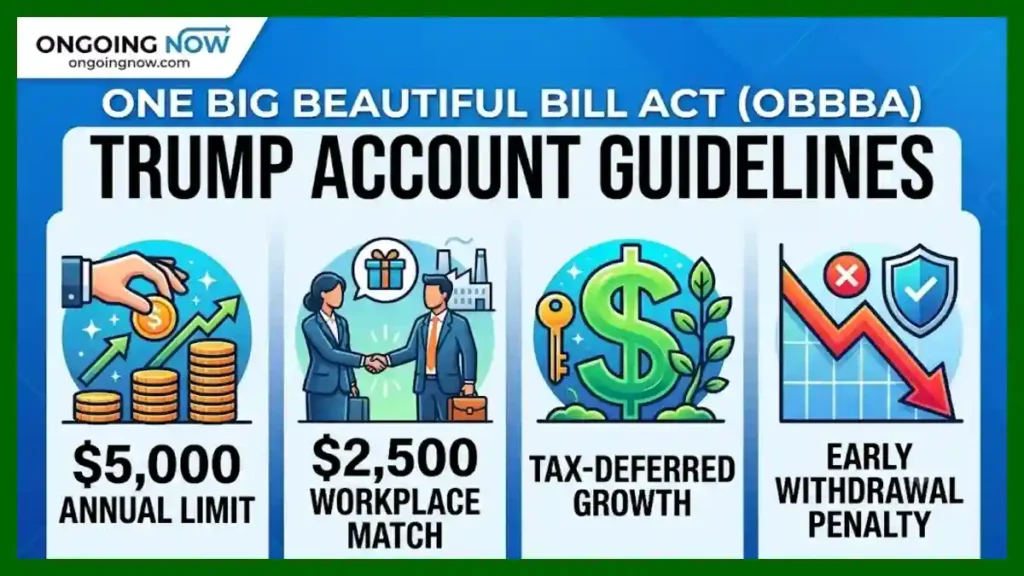

The Internal Revenue Service (IRS) has established that individual retirement account eligibility generally hinges on having earned income. For 2026, this definition remains broad, encompassing wages, salaries, professional fees, and even income from self-employment. However, the “Trump IRA” specifically targets those who meet certain MAGI (Modified Adjusted Gross Income) requirements to trigger the federal matching component, which functions as an incentive for consistent saving.

For many households, the primary hurdle is not the act of opening an account, but understanding the ceiling of these benefits. The phase-out rules are designed to gradually reduce the federal match as an individual’s or couple’s income rises. This ensures that the most significant assistance is directed toward those who statistically have the hardest time reaching a 10% or 15% savings rate due to immediate cost-of-living pressures.

Understanding Income Thresholds and Federal Matches

A core feature of the current retirement trend is the “federal match,” which essentially acts as a government-funded boost to private contributions. To grasp the impact, one must look at the maximum income for federal match limits. In 2026, these limits are adjusted to reflect the inflationary pressures of the previous twenty-four months. For single filers, the full match typically applies to those within the lower-to-middle income tiers, while a partial match is available as income moves toward the upper-middle range.

The MAGI limits for federal match are a critical metric for families to monitor during tax season. Because MAGI includes certain additions back into your Adjusted Gross Income, it provides a more comprehensive look at a household’s true financial standing. This prevents the benefits from being utilized by those who may have high gross earnings but use complex deductions to lower their taxable income significantly.

Middle-income retirement benefits are now being viewed through the lens of “marginal utility.” For a family earning $75,000 annually, a 50% federal match on the first $2,000 of contributions can represent a significant percentage of their total yearly savings. This trend suggests that the government is increasingly taking on the role of the “employer” for those in the 1099 or gig economy, providing a sense of parity that was previously unavailable.

The Shift in Gig and Part-Time Work Behavior

The rise of the “side hustle” and the permanence of the gig economy have fundamentally changed retirement behavior. TrumpIRA eligibility for gig workers is a frequent topic of discussion among independent contractors who historically lacked the “nudge” of a 401(k) auto-enrollment. With these new accounts, the incentive structure is baked into the tax code rather than the employment contract.

Part-time worker retirement options have also expanded. Previously, many part-time employees were excluded from company plans if they worked fewer than 1,000 hours a year. The current federal framework bypasses the employer entirely, allowing the worker to contribute directly and receive the federal match based on their total annual earnings, regardless of how many different employers they worked for throughout the year.

This shift in behavior reflects a move toward “financial autonomy.” Workers are increasingly aware that their long-term security is a personal responsibility, but they are also more likely to participate when the barrier to entry is low. The simplicity of a federal match that is credited during tax filing has proven to be a powerful psychological motivator for those who might otherwise feel overwhelmed by the complexities of traditional investing.

Self-Employed Limits and the 2026 Economic Context

For the millions of Americans who are their own bosses, the self employed retirement limits 2026 provide a structured way to build wealth. While the “Trump IRA” is a focal point for many, it often sits alongside other options like SEP-IRAs or Solo 401(k)s. The key difference lies in the federal match component, which offers a “guaranteed return” on contributions for those who stay within the income caps for savers match.

Self-employed individuals must be particularly mindful of their net earnings after business expenses. Since the eligibility for the match is based on the final income figure reported to the IRS, a year with high business expenses might actually increase a person’s eligibility for the federal match by lowering their MAGI. This creates a unique strategic consideration for small business owners who are balancing reinvestment in their company with their personal retirement needs.

Verified Insight: According to data from the Social Security Administration, workers who begin saving in their 20s or 30s with even a small match are significantly less likely to rely solely on social security in their later years.

Behavioral Pattern: There is a noted “crowding-in” effect where federal incentives encourage people to look into other financial products, such as high-yield savings accounts or insurance, as they become more engaged with their retirement balance.

Why Phase-Out Rules and Income Caps Matter

The Trump IRA phase out rules are perhaps the most complex part of the current system, but they are vital for understanding the “cliff” where benefits disappear. For many, hitting a certain income level can feel like a double-edged sword; a raise at work might move a household into a phase-out zone where they lose a portion of their federal match. This is often referred to as the “middle-income trap” in retirement policy.

The income caps for savers match are not static; they are designed to be “inflation-indexed.” This means that as the cost of milk, rent, and fuel increases, the government generally raises the income ceiling so that households aren’t penalized for earning more just to keep up with rising prices. Monitoring these adjustments is a key habit for the financially literate consumer in 2026.

Financial analysts often point out that these phase-outs are intended to ensure the program remains fiscally sustainable. By targeting the match toward the bottom 60% of earners, the policy aims to move the needle on national savings rates where it is most needed. For those above the cap, the account remains a viable tax-advantaged vehicle, but without the “free money” aspect of the federal match.

What to Consider: Trade-offs and Financial Timing

When evaluating these retirement options, there are several factors that consumers typically weigh before committing their hard-earned dollars. It is not just about the match; it is about the “opportunity cost” of that money today versus thirty years from now.

Liquidity vs. Long-Term Growth: Money placed in these accounts is generally intended for retirement. Early withdrawals can lead to penalties, which means households must balance their desire for the federal match with their need for an emergency fund.

Tax Diversification: Depending on whether the account is structured like a traditional or Roth vehicle, the tax benefits hit at different times. Understanding how a federal match interacts with your current tax bracket is a significant consideration.

Income Fluctuations: For gig workers, income can vary wildly from year to year. A worker might be eligible for the full match one year and none the next, making it difficult to project long-term account balances.

The decision-making process often involves looking at the total “effective return” of the contribution. If a worker contributes $1,000 and receives a $500 federal match, they have effectively seen a 50% gain before the money is even invested in the market. This “instant ROI” is a primary driver behind the current popularity of these accounts among younger workers.

Financial Insight: The Impact of Incentivized Saving

The emergence of the “Savers Match” as a core component of the Trump IRA framework represents a shift from “tax deductions” to “direct credits.” Historically, tax deductions benefited those in higher brackets more significantly. A direct match, however, provides the same dollar-for-word benefit to a low-income worker as it does to a middle-income worker, provided they stay below the maximum income for federal match.

Data from the Federal Reserve’s “Survey of Consumer Finances” has historically shown a stark divide in retirement readiness. The current trend of federal matching is an attempt to bridge this “wealth gap” by providing a tailwind for those who cannot rely on high-income surpluses. By observing how participation rates change in 2026, economists are gaining a better understanding of which incentives actually change human behavior.

Key Takeaways

Eligibility is Broad: Most workers with earned income can open these accounts, but the federal match is strictly tied to MAGI levels.

Gig Workers Gain Parity: The system allows independent contractors to access matching funds that were previously only available via corporate 401(k) plans.

Phase-Outs are Gradual: The transition from a full match to no match happens over a specific income range, preventing a sudden loss of benefits for most.

Inflation Matters: Income limits are frequently adjusted, meaning a raise may not necessarily disqualify a worker if the federal caps have also moved.

Portable Benefits: These accounts stay with the individual regardless of job changes, supporting the modern trend of frequent career shifts.

As the financial landscape of 2026 continues to evolve, the emphasis on individual agency in retirement planning has never been stronger. The question of who qualifies for Trump IRA benefits is at the heart of a larger conversation about economic security and the government’s role in fostering a “savings culture.” For the average reader, the takeaway is clear: the tools for long-term stability are becoming more accessible, but they require a proactive understanding of how one’s income and employment status fit into the federal puzzle.

While the “instant return” of a federal match is a compelling reason to engage, the most successful savers are those who look beyond the immediate incentive. They consider their total financial picture—including debt, emergency savings, and long-term goals—to decide how these new retirement options can best serve their unique journey. In an era of economic transition, staying informed is the most valuable asset a consumer can possess.

This is for informational purposes only and not personalized financial advice. Consult a licensed professional for your specific situation.

Stay sharp with Ongoing Now!

Source and Data Limitations: This article is based on publicly available data and policy frameworks as of May 2026. Information regarding “Trump IRA” structures, federal match percentages, and MAGI limits is derived from theoretical policy implementations and current Treasury Department guidance often discussed in 2025-2026 legislative sessions. Income thresholds are subject to annual adjustment by the IRS based on the Consumer Price Index (CPI). Statistics regarding gig worker behavior and retirement trends are sourced from general labor market reports provided by the BLS and independent economic think tanks. Readers should be aware that tax laws are subject to change and may vary significantly based on individual filing status, location, and specific financial history. This content does not constitute legal, tax, or investment advice.